Management

Discussion and Analysis

Industry Trends and Business Overview

Driving Growth with Purpose in a Changing World

The Management Discussion and Analysis provides an integrated perspective on Lupin’s performance and strategic direction in FY26, bringing together our operational, financial, and sustainability outcomes within the context of a changing global healthcare landscape. Our purpose – catalyzing treatments that transform hope into healing – serves as our North Star, shaping decisions and actions with a clear focus on delivering enduring value for patients and stakeholders.

FY26 was a defining year in which disciplined execution, strategic clarity, and sustained investments translated into strong performance. We accelerated momentum across key markets, advanced our innovation agenda, and made meaningful strides in our ESG priorities, strengthening resilience in an evolving landscape.

These outcomes reflect a more focused business with greater strategic agility, better positioned to deliver sustainable growth and improved patient outcomes.

Moderating Global Growth and Evolving Healthcare Dynamics

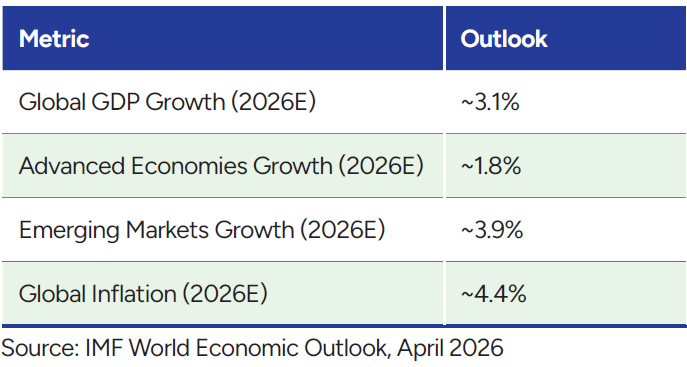

According to the International Monetary Fund (IMF), global economic growth is projected at 3.1% in 2026 and 3.2% in 2027, slower than the 3.4% pace in 2025 (IMF World Economic Outlook, April 2026). Growth in advanced economies is expected to remain stable at around 1.8% (IMF World Economic Outlook, April 2026), while emerging markets and developing economies are projected to grow at 3.9%, moderating from 4.4% in 2025 (IMF World Economic Outlook, April 2026). Global inflation is forecast to rise, with headline inflation increasing from 4.1% in 2025 to 4.4% in 2026 before falling back to 3.7% in 2027. This upward revision in 2026 reflects anticipated pressures from energy and food prices.

Global Economic Outlook at a Glance

Amid these shifts, the pharmaceutical sector remains relatively resilient, supported by the essential nature of healthcare demand. Rising pharmaceutical consumption is primarily driven by improved access in emerging markets, while the industry’s value growth is increasingly shaped by complex generics, biosimilars, specialty therapies, and advanced delivery technologies. These trends underscore a dual evolution – expanding patient access alongside a transition toward more complex, higher-value therapies.

For Lupin, these shifts reinforce our strategy of building a more differentiated, complexity-led portfolio. We are focused on sharpening our specialized offerings, reinforcing manufacturing reliability, preserving regulatory credibility, and broadening the reach of high-quality medicines across geographies.

Strategic Agility in a Transforming Market

Global Pharmaceutical Industry – Structural Growth Anchored in Innovation and Access

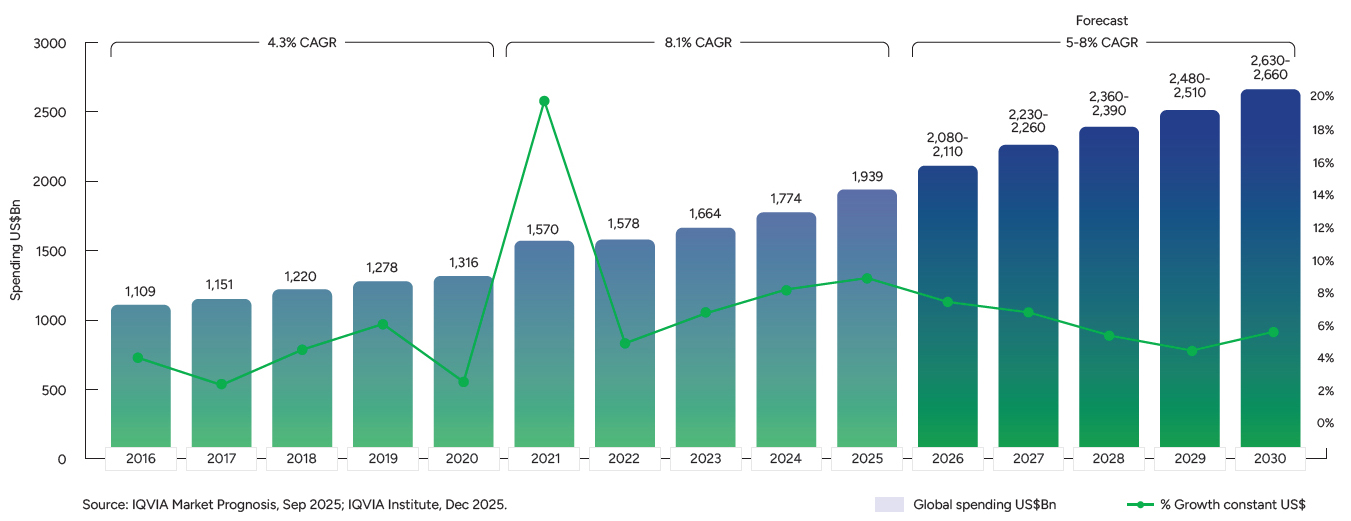

TThe global pharmaceutical industry continues to benefit from sustained healthcare demand, expanding access to medicines, and accelerating scientific innovation. Worldwide pharmaceutical spending is projected to reach USD 2.08-2.11 trillion in 2026, with growth expected at a 5-8% compound annual rate through 2030, materially outpacing global economic growth (IQVIA Institute, Global Medicine Use Trends, 2026).

USD 2.08-2.11 Tn

Global Pharma Market Size (CY 2026E)

Global medicine market size and growth including estimated COVID-19 vaccine and therapeutic spending, 2016-2030

Global Pharmaceutical Market – Usage and Value Outlook

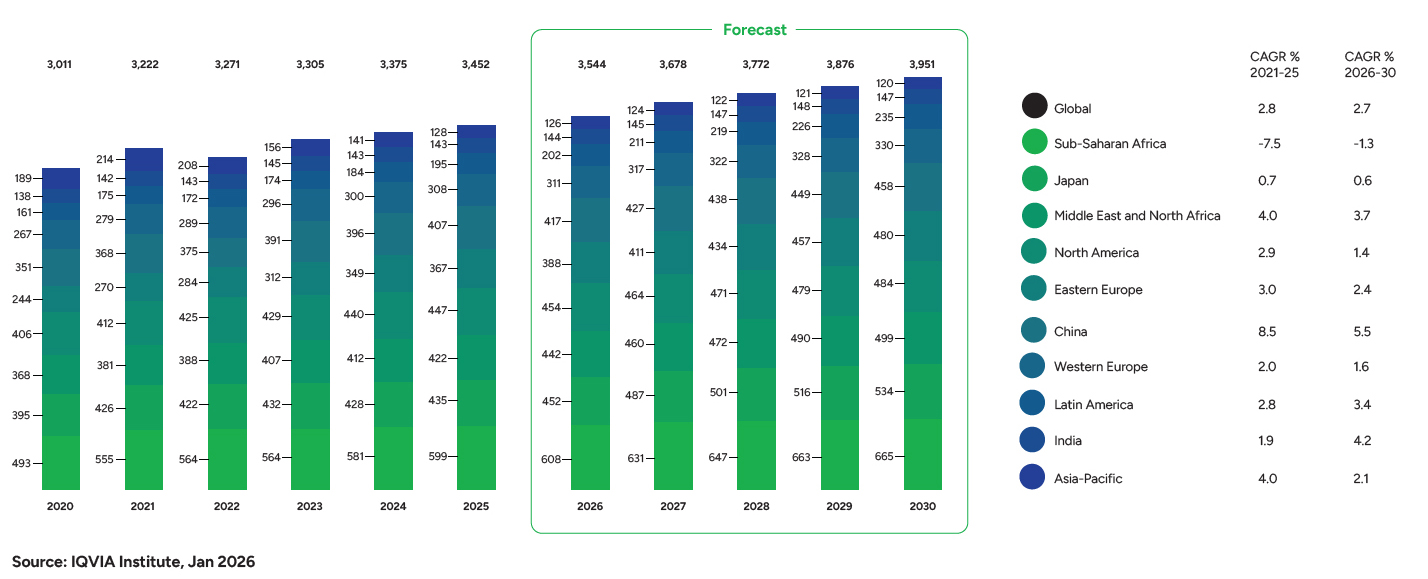

The global consumption of medicines is expected to reach four trillion Defined Daily Doses (DDDs) by the end of the decade, driven by expanded healthcare access in emerging markets, aging populations and deeper chronic disease treatment. (IQVIA Institute, 2026 Forecast).

Historic and projected use of medicines by region, Defined Daily Doses (DDD) in billions, 2020-2030

Value growth is increasingly driven by innovation-led therapies, complex generics, biosimilars, specialty products, and differentiated platforms. These trends point to a more balanced global growth model, where broader access and advancing innovation together underpin the pharmaceutical sector’s longterm resilience. (Statista, Pharmaceuticals Market Outlook).

Developed and Emerging Markets as Complementary Growth Engines

Developed and Emerging Markets continue to play distinct but complementary roles in global pharmaceutical growth. Developed Markets, led by North America, remain the largest contributors by value, driven by the rapid adoption of innovative and specialty therapies.

Emerging Markets across Asia, Latin America, Africa, and the Middle East are expected to record mid-to-high single-digit growth, backed by increasing healthcare investments, expanding insurance coverage, and improved access to essential medicines (IQVIA Institute, Global Medicine Use Trends; Statista, Worldwide Pharmaceuticals Outlook). This creates a differentiated growth landscape across regions, with market strategies varying by geography, portfolio mix, and access priorities.

Therapeutic Focus Areas Shaping Global Demand

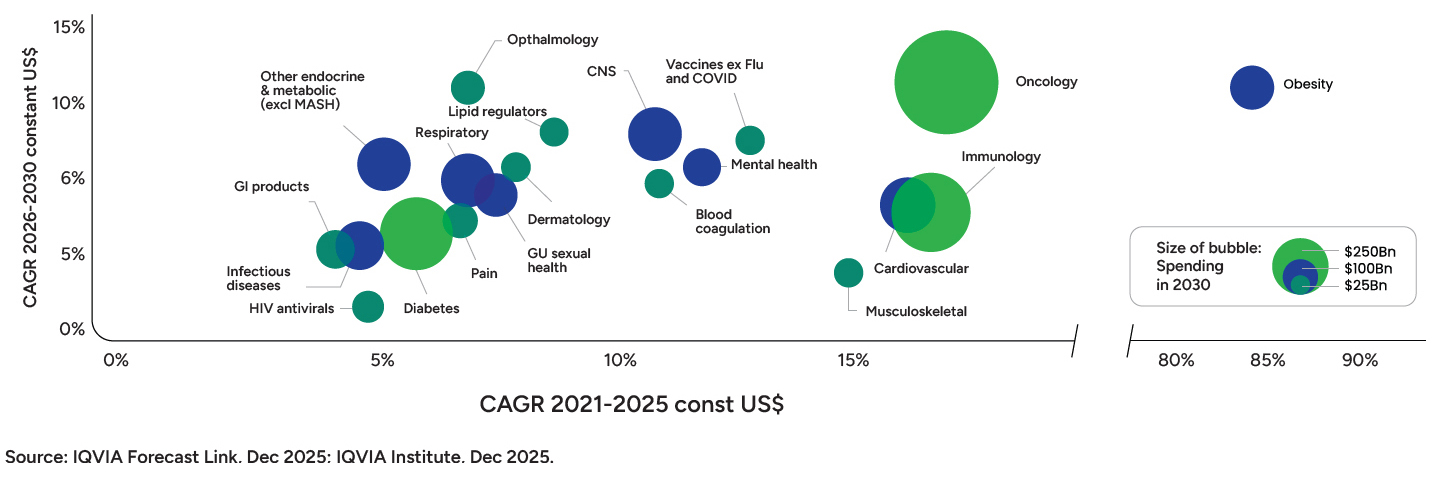

Global pharmaceutical expansion continues to be centered on therapies that address large and rising disease burdens. Oncology remains the largest therapeutic segment, with global spending projected to exceed USD 441 billion by 2029, driven by precision medicine, immunotherapies, and next-generation biologic platforms (IQVIA Forecast).

Cardiometabolic diseases and obesity have emerged as powerful growth drivers. GLP-1-based treatments generated approximately USD 130+ billion in global sales in 2025, with obesity-focused therapies seeing rapid adoption as treatment paradigms evolve and access expands across geographies (IQVIA; J.P. Morgan Research).

Innovation in immunology, Central Nervous System (CNS) disorders and rare diseases is also shifting the market toward more differentiated, higher-value therapies. Together, these therapeutic segments reflect a market increasingly shaped by disease burden, differentiated science, and long-term treatment needs.

Global historic and forecast growth for top 20 therapy areas, constant USD, 2021-2030

Portfolio Renewal and the Evolving Value Mix

The current decade marks a broad phase of portfolio renewal in the global pharmaceutical industry. Between 2025 and 2030, branded medicines, accounting for approximately USD 230 billion in annual sales, are expected to transition beyond exclusivity, with biologics comprising a significantly larger share of this cohort than in earlier cycles.

This transition should expand patient access through greater use of generics and biosimilars, while placing increased focus on strong development capabilities, regulatory execution, and reliable manufacturing. (IQVIA Institute, The Rules of Loss of Exclusivity Are Being Rewritten; Drug Discovery News, Blockbuster Drugs Face a Major Patent Cliff in 2026).

USD 230 Bn

Estimated annual sales of brands transitioning beyond exclusivity (2025-2030)

India – A Growth Market and Global Pharmaceutical Capability Hub

India remains one of the world’s fastest-growing major economies and a key driver of global growth, with the IMF projecting India’s GDP growth at 6.5% in 2026. This is supported by strong domestic demand, policy continuity, and sustained investment (IMF World Economic Outlook, April 2026 update).

The country’s economic expansion is broad-based, anchored in consumption growth, infrastructure spending, digitalization, and the formalization of the economy. While inflation is expected to remain within a manageable range, the outlook requires continued monitoring given geopolitical uncertainty, energy price volatility, currency movements, and food-price risks. This macroeconomic environment remains supportive of healthcare investment, public health spending and long-term pharmaceutical demand (IMF World Economic Outlook, April 2026).

The Indian pharmaceutical market is estimated at approximately USD 60 billion (including exports) in 2026, with long-term projections indicating growth toward USD 130 billion by 2030, driven by rising healthcare penetration, chronic disease prevalence, and wider insurance coverage (PIB, India Pharma 2026). Alongside this expanding domestic base, India’s strong manufacturing foundation continues to support the sector’s shift from volume-led growth to greater strategic depth and global relevance.

India is one of the world’s most important suppliers of affordable medicines, accounting for nearly 20% of the global generic medicine supply by volume and a significant share of global vaccine demand (PIB, India Pharma 2026). This position is reinforced by a robust manufacturing base, regulatory experience, and scientific talent, including the highest number of U.S. FDA-approved plants outside the United States and more than 2,000 WHO-GMP-certified facilities.

Government initiatives such as Production Linked Incentive schemes, bulk drug parks, technology upgradation programs, and targeted support for biopharmaceutical research continue to enhance domestic manufacturing depth and innovation capability. By enabling capacity expansion, technology adoption, and specialized infrastructure, these initiatives are further strengthening India’s position as a global pharmaceutical manufacturing leader that delivers highquality, cost-competitive medicines at scale (Department of Pharmaceuticals, India Pharma 2026).

Looking Ahead

The global pharmaceutical market is positioned for sustained long-term growth, driven by rising medicine usage, therapy evolution, portfolio renewal, and widening patient access in emerging economies.

Strategic Trends Shaping the Industry

The pharmaceutical sector is amid a structural transformation that extends well beyond cyclical change. Advances in science, rising healthcare expectations, regulatory evolution, supply chain uncertainty, and rapid digital adoption are reshaping how medicines are developed and delivered. AI and digital technologies are being leveraged to enhance efficiency and productivity across the value chain. These shifts are driving more complex, resilient, and patient-centric business models.

Shift Toward Complex Generics and Specialty

Persistent pricing pressure in commoditized oral solids is accelerating the industry’s shift toward complex generics, specialty products, and differentiated dosage forms, including injectables, inhalation therapies, peptides, and niche platforms. Higher development complexity and regulatory scrutiny are raising barriers to entry and favoring companies with scientific depth, advanced manufacturing, and robust quality systems.

GLP-1 Therapies Expand the Market

The rapid adoption of GLP-1 therapies has enhanced the reach and visibility of cardiometabolic treatment, especially across diabetes and obesity. As key molecules approach patent expiry, the segment is expected to transition from innovator-led growth to broader participation from differentiated generics and complex formulations and greater access across markets. This creates opportunities for companies with formulation depth, supply reliability, and disciplined market access capabilities.

Patent Expiries Accelerate Portfolio Renewal

The industry is entering a significant patent cliff cycle, with several blockbuster medicines expected to lose exclusivity through the second half of the decade. This will accelerate generic and biosimilar adoption while intensifying competition in high-value therapeutic categories. Companies with strong development, regulatory, and manufacturing capabilities will be best positioned to benefit.

Biosimilars and Advanced Modalities Gain Momentum

As healthcare systems seek cost-effective alternatives, biologics account for an increasing share of pharma innovation and spending, creating parallel demand for biosimilars. Evolving regulatory pathways – including greater clarity on interchangeability and biosimilar guidelines in key markets – are expected to support adoption. At the same time, advanced modalities such as long-acting injectables, antibody-drug conjugates, oligonucleotides, peptides, and high-containment products will require specialized capabilities, reinforcing the importance of technology, talent, and compliance excellence.

Quality and Compliance Become Competitive Advantages

Export-oriented pharma models are facing greater regulatory scrutiny, higher compliance costs, and more demanding quality governance expectations. Increasingly, sustainable margins depend as much on quality systems, inspection readiness, and reliable supply as they do on cost competitiveness.

Supply Resilience Becomes Strategic

Supply chain volatility remains a defining challenge for the industry. API and input-cost inflation, logistics disruptions, freight volatility, geopolitical risks, and sourcing concentration have increased the need for robust supply networks. Companies are responding through supplier diversification, regional manufacturing, backward integration, and stronger procurement governance. Supply chain strategy is increasingly focused on reliability, traceability and continuity of supply rather than cost alone.

CRDMO Opportunity Continues to Expand

Outsourcing across the value chain remains a significant structural trend. Contract Research Organizations (CROs), Contract Research, Development and Manufacturing Organizations (CRDMOs), and Contract Development and Manufacturing Organizations (CDMOs) continue to support global companies in accelerating development, managing costs, and accessing specialized capabilities. Long-term demand remains strong in high-containment APIs, biologics, peptides, Antibody-Drug Conjugates (ADCs), oligonucleotides and complex chemistry, favoring technically capable and compliant partners.

AI Moves to Scale

AI and digital transformation are scaling rapidly across the enterprise, spanning R&D, clinical trials, manufacturing, quality, supply chain, and commercial operations. Advanced analytics, automation and AI-enabled platforms are improving trial design, accelerating decision-making, strengthening quality oversight, optimizing manufacturing, and improving commercial effectiveness. As adoption increases, responsible AI governance, cybersecurity, data integrity and change management, and robust data governance are becoming essential to realizing AI’s full potential.

Governments Push for Pharmaceutical Self-Reliance

Across markets, governments are intensifying their focus on domestic pharmaceutical capability, supply security, and reduced reliance on concentrated sources of key inputs. Policy initiatives – including production-linked incentives, bulk drug parks, technology upgrades and local manufacturing support – are strengthening domestic ecosystems for APIs, key starting materials, and essential medicines. For India, these initiatives reinforce its position as a global pharmaceutical manufacturing and innovation hub.

Healthcare Extends Beyond Medicines

Pharma companies are extending their role beyond medicines into broader healthcare ecosystems. Diagnostics, medtech, digital health, connected care, patient-support programs, and adherence platforms are becoming increasingly relevant as healthcare systems focus on prevention, chronic disease management, and outcomes. This shift is creating more integrated models of care and deeper engagement with patients, providers, and payers.

Sustainability and Responsible Operations Become Strategic Priorities

Sustainability and ESG priorities are increasingly shaping how companies manage risk, earn stakeholder trust, and deliver sustainable long-term value. Climate action, responsible sourcing, and supply chain transparency are becoming core expectations of regulators, investors, customers, and communities. Companies that embed sustainability into strategy and operations will be better positioned to strengthen long-term value creation and stakeholder confidence.

Global Expansion Accelerates

Companies globally are leveraging cross-border investments, acquisitions, partnerships, and capacity creation outside their home markets to fortify market access and supply security. These strategies improve customer proximity, diversify manufacturing networks and provide access to specialized technologies while strengthening supply chain resilience.

Funding Pressures Challenge Access Markets

Budgetary pressures affecting global health programs, including USAID-supported initiatives, may reduce funding for certain public health programs, donor-funded procurement, and innovation initiatives. This may affect institutional demand in vulnerable markets, reinforcing the importance of diversified market access models and disciplined participation in tender-led programs

A Strategic Inflection Point for the Sector

The global pharma industry is at a critical juncture. Scientific advances, evolving regulation, supply chain realignment, and affordability pressures are reshaping the competitive landscape. For Lupin, these trends reinforce the strategy we have pursued over many years: building differentiated scientific capabilities, strengthening manufacturing excellence and expanding access to high-quality medicines.

Opportunities and Threats

Opportunities – Harnessing Structural Industry Transitions

Complex Generics, Specialty Products, and Differentiated Platforms

Lupin’s focus on complex generics, respiratory therapies, injectables, peptides, specialty products, and differentiated delivery platforms positions us competitively in higher-value segments with stronger barriers to entry. Our strengths in product development, drug-device combinations, quality systems, and manufacturing enable us to compete selectively in opportunities where technical expertise and reliable execution matter most.

GLP-1, Obesity, and Cardiometabolic Opportunities

The rapid growth of GLP-1 therapies is opening opportunities across diabetes, obesity, and broader cardiometabolic care. Lupin’s established presence in chronic therapies, including market leadership in cardio-metabolic segments, formulation development, and complex products, provides a solid base to evaluate opportunities in peptides, differentiated delivery formats, and follow-on products through disciplined portfolio selection.

Biosimilars and Advanced Modalities

As biologics gain share in global pharmaceutical spending, biosimilars are becoming important drivers of affordability and access. Evolving regulatory pathways are broadening market opportunities. Our integrated capabilities across development, manufacturing, regulatory affairs, and commercialization position us to participate selectively in high-complexity biosimilar opportunities.

Contract Research, Development and Manufacturing Opportunities

Growing demand for technically capable and compliant development and manufacturing partners creates attractive opportunities for Lupin Manufacturing Solutions. The rising demand for credible, compliant, and technically capable development and manufacturing partners enables us to reinforce Lupin’s role in higher-value outsourcing. Our capabilities in complex chemistry, high-containment APIs, peptides, biologics, antibody-drug conjugates, and oligonucleotides position us well in specialized outsourcing segments where quality, scientific expertise, and execution are key differentiators.

Emerging Markets Growth and Access-Led Expansion

Expanding healthcare coverage, public health investment, and treatment of chronic diseases in emerging markets present growth opportunities for us. Our broad portfolio, established presence, and reliable supply chain position us to expand reach through locally relevant products and longstanding institutional partnerships.

USD 120+ Bn

Expected spending growth in Pharmerging markets (IQVIA Institute, Global Medicine Use Trends 2026)

India as a Global Pharmaceutical Manufacturing and Capability Hub

India is central to Lupin’s growth agenda, both as a domestic market and as a global capability base. Growing healthcare demand, policy support, and India’s manufacturing ecosystem continue to strengthen both our domestic business and our global development and supply platform.

Supply Chain Diversification and Resilience

Supply chain volatility has highlighted the importance of reliable sourcing, backward integration, inventory planning, and manufacturing flexibility. Our continued investments in supply resilience enhance continuity, reduce operational risk, and strengthen customer confidence across markets.

AI, Digital Transformation, and Productivity Enhancement

Digital tools, advanced analytics, and GenAI are improving productivity across R&D, clinical development, manufacturing, quality, supply chain, and commercial operations. Our digital initiatives are strengthening forecasting, accelerating decision-making, enhancing quality oversight, and improving manufacturing and commercial effectiveness.

Sustainability and Responsible Operations

Sustainability has become a competitive differentiator for customers, regulators, investors, and communities. Our focus on energy efficiency, water stewardship, waste management, responsible sourcing, and supply chain transparency strengthens operational resilience while reinforcing stakeholder trust.

Expansion Across the Healthcare Continuum

Healthcare is moving beyond medicines toward more integrated models of care. We continue to expand our healthcare ecosystem through diagnostics, digital health, patient-support programs, and disease management initiatives. These adjacencies augment our chronic and specialty portfolios while improving patient outcomes.

Outbound Expansion and Building a Global Footprint

Cross-border investments, partnerships, and acquisitions continue to strengthen market access, regulatory proximity, and local presence in priority markets. Our disciplined approach to international expansion enhances portfolio depth, provides access to specialized capabilities, and supports sustainable long-term growth across regulated and emerging markets.

Threats – Managing Risk in a Complex Environment

The evolving pharma landscape presents a range of strategic and operational risks, including regulatory, commercial, supply chain, and technology-related challenges. Our Enterprise Risk Management framework, quality systems, digital controls, supply chain governance, disciplined portfolio choices, and strong compliance are designed to help anticipate, monitor, and mitigate these risks.

Regulatory Scrutiny and Export Model Pressure

Lupin’s regulated market businesses operate under stringent expectations regarding quality systems, data integrity, inspection readiness, and supply continuity. Any regulatory observations, delayed approvals or site-related disruptions can affect launch timelines, market access, and customer confidence. We mitigate these risks through proactive regulatory engagement, continuous quality improvement, and sustained investment in manufacturing excellence.

Pricing, Reimbursement and Affordability Pressure

Pricing pressure remains an ongoing challenge in mature markets, particularly in commoditized generics and tender-led portfolios. Changes in reimbursement frameworks, payer consolidation, and cost-containment measures can affect margins. Our focus on complex products, differentiated portfolios, and disciplined cost management reduces our exposure to pure pricebased competition.

Supply Chain Volatility and Input Cost Inflation

API and input cost inflation, logistics disruptions, freight volatility, and sourcing concentration can adversely impact margins, inventory planning and service levels. These risks can also influence launch readiness and customer commitments if supply continuity is disrupted. We continue to prioritize supplier diversification, procurement discipline, backward integration, and business continuity planning to improve supply resilience.

Global Health Funding and Institutional Market Pressure

Budgetary pressure on donor-funded healthcare programs and public health procurement can affect institutional demand in access-led markets. This may result in volatility in tender volumes, pricing, receivables, and demand visibility. We address these risks through disciplined tender participation, diversified market access models, and close monitoring of institutional channels.

Digital, Cybersecurity, and Data Privacy Risks

As Lupin extends digital systems across R&D, manufacturing, quality, supply chain, and commercial operations, there is increased exposure to cybersecurity and data privacy risks. System disruption, unauthorized access, data integrity issues, regulatory non-compliance or cyber-attacks can affect operations and stakeholder trust. We continue to advance cybersecurity, access controls, responsible AI governance, and data protection frameworks across the enterprise.

Execution Risk in Complex and Specialty Portfolios

Complex generics, biosimilars, specialty products, and advanced modalities offer stronger opportunities but carry higher execution risk. Longer development cycles, specialized manufacturing processes, demanding regulatory requirements, and technology transfer complexity can impact launch timing, cost recovery, and returns. Our disciplined approach to portfolio selection, technical readiness, and program execution is designed to manage these risks.

Competitive Intensity from Patent Cliff and Genericization

As more high-value products lose exclusivity, competition is expected to intensify, increasing the risk of rapid price erosion following launch. Success will depend on selecting the right opportunities, achieving timely approvals, and maintaining reliable supply. Speed to market and lifecycle management will remain important competitive differentiators.

Geopolitical, Currency, and Market Access Risks

Lupin’s presence across multiple geographies exposes the business to currency movements, trade barriers, localization requirements, policy changes, geopolitical disruption, and evolving market access requirements. These factors can affect procurement costs, pricing, supply continuity, and profitability. We mitigate these risks through active treasury management, regional planning, and ongoing regulatory monitoring.

Talent and Capability Availability

Lupin’s growth in complex products, biologics, advanced manufacturing, digital technologies, AI, cybersecurity, and global quality systems depends on specialized talent. Competition for these skills can affect innovation, operational execution, and compliance. We continue to invest in leadership development, capability building, succession planning, and future-ready talent.

Segment-Wise Performance

FY26 was marked by disciplined execution and the enhancement of capabilities across our diversified business portfolio. We delivered consistent performance across segments by leveraging our global reach and balanced therapy mix while reaffirming our commitment to portfolio quality, reliability, and rigorous operational discipline. Our investments in portfolio quality, manufacturing excellence, and regulatory readiness continue to cement our long-term competitive position.

We outperformed all our targets, delivering strong financial and operational results while achieving significant milestones this year. Our performance in key markets including the U.S., India, Other Developed Markets, and the turnaround in Brazil, validates our commitment to perseverance and disciplined execution. We also continued to enrich our innovation pipeline across multiple technology platforms.

U.S. – Advancing Portfolio Quality and Market Position

Our U.S. business was driven by a more differentiated portfolio, supported by high-value, exclusivity-driven products such as Mirabegron Extended-Release Tablets, Tolvaptan Tablets, and Risperidone. Complex generics, respiratory products, select specialty channel offerings, and biosimilars also contributed to growth, improving revenues, quality, and profitability.

Pricing pressures persisted in commoditized oral solid segment. This was offset by favorable product mix, differentiated products, and disciplined portfolio management.

The year reinforced our strategy of focusing on products where scientific capability and execution create sustainable differentiation.

Ongoing remediation efforts, quality system upgrades, and proactive engagement with the U.S. FDA bolstered our manufacturing facility preparedness and helped lower execution risk. These actions support future product approvals, raise launch confidence, and deepen customer trust in a highly regulated market.

India – Sustaining Leadership Through Breadth and Depth

Our India Formulations business delivered another strong year, contributing around 30% of global revenues while continuing to outperform the Indian Pharmaceutical Market. Growth was driven by our leadership in chronic therapies, including cardiology, diabetes, respiratory, and gastroenterology. Sustained prescription growth, rising chronic disease prevalence, and longer treatment durations continue to support long-term growth.

Our established brands, deep physician relationships, and reliable product availability strengthened our competitive position. Investments in field-force productivity, capability building, and segmentation enhanced engagement with healthcare professionals, while digital and hybrid channels improved reach and effectiveness. We also expanded our presence across Tier-2 and Tier-3 markets through broader distribution, targeted portfolios, and patient-support initiatives, driving long-term franchise growth.

Overall, this year demonstrated our ability to combine scale with adaptability, showcasing India as a stable and resilient foundation within our global operations.

Other Developed Markets – Consistent Execution in Regulated Geographies

Our Other Developed Markets delivered consistent growth, supported by focused portfolio choices, disciplined execution, and reliable supply. We maintained a differentiated portfolio centered on niche generics and specialty medicines while participating selectively in tender and institutional opportunities.

The acquisition of VISUfarma expanded our ophthalmology platform and commercial presence across Europe, while Renascience further strengthened our differentiated portfolio.

Our compliance track record, regulatory agility, and supply reliability continue to differentiate Lupin as a trusted partner across developed markets.

Emerging Markets – Access-Led Expansion with Portfolio Customization

Our Emerging Markets business continued to grow, supported by rising healthcare access, new product launches, and expanding private-market and institutional businesses. Growth across South Africa, Brazil, Mexico, and the Philippines reflected locally relevant portfolios, deeper institutional engagement, and dependable supply.

We continued to tailor our portfolio to local healthcare needs, reinforcing our long-term commitment to these markets.

Active Pharmaceutical Ingredients – Strengthening Supply and Integration

Our API business remains a critical component of Lupin’s integrated operating model, ensuring a reliable, quality-assured supply for our formulations business. During FY26, we improved capacity utilization, furthered backward integration, and enhanced operational efficiency.

External customer deliveries complemented internal supply while ongoing investments in compliance and process excellence enhanced competitiveness and execution reliability.

API Plus – Institutional Access and Public Health Channels

API Plus comprises select API business opportunities and institutional sales channels, including engagement with public health agencies, WHO-linked programs, healthcare bodies, and tender-led markets. These channels are characterized by procurement cycles in which quality, regulatory compliance, and supply reliability are critical.

The business navigated funding cycles, institutional demand patterns, and procurement dynamics while supporting Lupin’s broader access agenda. We remained focused on strengthening participation in API-linked and institutional opportunities where dependable supply and compliance strength are key requirements.

Lupin Manufacturing Solutions – Building Specialized Manufacturing Partnerships

Lupin Manufacturing Solutions (LMS) continues to build specialized contract development and manufacturing partnerships with global customers. During FY26, the business expanded capabilities across complex chemistry, high-potency APIs, peptides, and specialized manufacturing processes.

Its focus on quality, scientific capability, and execution enables selective participation in technically demanding manufacturing opportunities and fortifies Lupin’s position in global CDMO and CRDMO value chains.

Outlook

Looking ahead, the global pharmaceutical operating environment is expected to remain attractive, while becoming increasingly capability-driven. Growth will continue to be supported by rising healthcare demand, scientific innovation, expanding access to medicines, and the shift toward complex and differentiated therapies. Success will increasingly depend on scientific capability, regulatory excellence, manufacturing reliability, and disciplined execution.

For Lupin, this reinforces the strategy we have pursued over many years: investing in differentiated capabilities, strengthening operational excellence, and allocating capital with discipline. We will continue to focus on opportunities where our scientific, manufacturing, regulatory, and commercial strengths create sustainable competitive advantage.

India will remain a core pillar of Lupin’s growth, supported by strong macroeconomic fundamentals, rising healthcare penetration, and continued policy support for pharmaceutical manufacturing and innovation. Growing chronic disease prevalence, expanding insurance coverage, and greater emphasis on long-term care will continue to support demand.

We view India as both a major growth market and a global capability hub, with continued focus on strengthening our brands, expanding market reach, enhancing digital engagement, and delivering high-quality medicines.

In developed markets, growth will continue to be driven by differentiated products, compliance excellence, and supply reliability. While pricing pressure in commoditized segments is expected to persist, our focus on portfolio quality, disciplined execution and differentiated, launches positions us well.

Emerging markets will remain an important source of growth, supported by improving healthcare access, evolving treatment patterns, and increasing demand for affordable, high-quality medicines.

Across our businesses, we will continue to prioritize quality, digital capabilities, supply chain resilience, and manufacturing excellence while expanding our portfolio of complex and specialty medicines. API Plus and Lupin Manufacturing Solutions will further enhance our integrated capabilities and support future growth. As the operating environment evolves, our focus will remain unchanged: disciplined execution, responsible growth, and creating long-term value for patients, partners, and shareholders.

Risks and Concerns

We view effective risk management as a core enabler of sustainable growth and long-term value creation. Our operating environment is defined by macroeconomic volatility, an evolving regulatory landscape, dynamic patient expectations, climate considerations, and rapid technological progress.

Against this backdrop, we view risk not just as an exposure to be mitigated but as a vital diagnostic tool that sharpens strategic focus, enhances organizational readiness, and drives more effective decision-making.

In FY26, we further strengthened our Enterprise Risk Management framework to ensure early identification of emerging developments and proactive action to address these risks. Our approach integrates strategic, financial, operational, and compliance risks with evolving environmental, social, geopolitical, and technology related considerations. This integrated perspective supports consistent monitoring, escalation, and mitigation across the organization while enabling us to navigate complexity without losing sight of our long-term objectives.

Risks Categorization

To ensure structured oversight and timely response, we classify risks across four broad and inter-connected categories – Strategic Risks, Operations Risks, Emerging Risks, and Systemic Risks. This categorization helps us to assess risks based on their nature, potential impact, and relevance to business continuity, growth priorities, and stakeholder expectations.

To improve early risk identification and responsiveness, we are bolstering our risk analytics capabilities by introducing real-time dashboards and predictive models. These initiatives are overseen by our cross-functional Risk Management Council, which plays a central role in surfacing early signals, enabling coordinated dialogue, and aligning actions with strategic priorities across functions.

Our experience during the year reaffirmed that resilience is built through anticipation, preparedness, and continuous improvement. By embedding risk awareness into execution and decision making across the enterprise, we continue to strengthen our ability to pursue growth opportunities responsibly while ensuring sustainable value creation.

Read more about Lupin’s risk portfolio and mitigation strategies in the Enterprise Risk Management chapter on page 184.

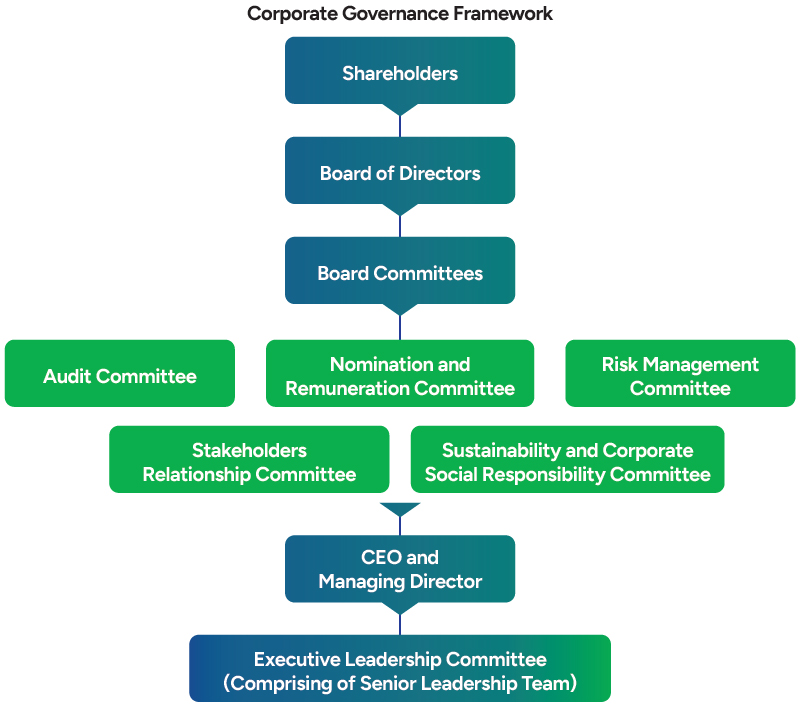

Internal Control Systems and Their Adequacy

At Lupin, our internal control systems are central to how we operate responsibly and deliver consistent performance. These controls are embedded across our organization and support effective decision-making, regulatory compliance, and accountability. The framework is designed in alignment with global best practices and covers financial reporting, operational effectiveness, compliance management, information security, and ethical standards. It is dynamic in nature and continues to evolve in response to changes in the operating environment, regulatory requirements, and emerging risks.

Oversight of internal controls is provided by our Board through the Audit Committee, Risk Management Committee, and other relevant committees. These committees, supported by a risk-based internal audit function, review the adequacy and effectiveness of controls across key business processes, financial systems, IT infrastructure, compliance mechanisms, and ESG-related practices. Internal audits are conducted across geographies and functions, with findings reviewed and monitored to ensure timely closure.

Ethical conduct is an integral part of our control environment. Our Code of Business Conduct and Ethics sets clear expectations for employees and partners and is supported by a confidential Ombudsperson platform and whistle-blower mechanism. These channels enable concerns to be raised safely and addressed promptly. We have also integrated ESG-related controls into our governance framework through Board-level and executive-level oversight structures. This ensures that matters such as climate considerations, data privacy, responsible sourcing, and human rights are embedded within business operations and disclosures.

We will continue to strengthen our internal control systems with greater use of digital tools, regulatory intelligence, and risk analytics. Furthermore, continuous control monitoring will be emphasized to enhance consistency, transparency, and accountability.

Financial Performance

FY26 showcased improved financial performance, with revenue growth accompanied by stronger margins, driven by a better portfolio mix, and operational efficiency. Our consolidated revenues increased by 23.1% year-on-year to INR 279,580 Mn, supported by growth across select geographies and product categories. EBITDA for the year rose by 68.6%, with EBITDA margins improving by 33.6%, while Profit Before Tax increased by 71.2%, resulting in a meaningful improvement in overall profitability compared to the previous year.

Our revenue growth was driven by traction in select complex and differentiated products, supported by consistent performance across our core businesses. We prioritized sustainability of revenue over short-term volume, aligning commercial efforts with products and markets where we see long-term relevance. Pricing pressure persisted in certain mature markets, which reinforced our focus on portfolio mix and execution.

Operational performance benefited from portfolio optimization, better pricing realization in niche segments, and cost management across manufacturing and supply chain operations. Higher capacity utilization at key facilities and tighter control over fixed costs supported improvements in operating leverage, contributing to stronger EBITDA margins.

Our investments in future growth were evident in research and development expenditure, which stood at INR 20,631 Mn, representing 7.5% of sales. This reflects our commitment to strengthening pipelines in respiratory, complex injectables, and biosimilars and is intended to support medium- to long-term growth, particularly in regulated markets.

Return on Capital Employed (ROCE) improved to 28.4%, underscoring efficient asset utilization, disciplined working capital management, and healthy operating cash flows. We maintained a net cash position, enhancing both, the strength of our balance sheet and financial flexibility.

Overall, this year demonstrated our ability to translate strategic priorities into measurable financial outcomes, providing a solid base as we plan the next phase of growth.

Read more details on our financial performance in the Financial Capital chapter on page 95.

Material Developments in Human Resources

Our Human Capital agenda is focused on building a future-ready organization capable of supporting sustained growth in a dynamic healthcare landscape. We continued to invest in strengthening our talent pipeline, enhancing workforce well-being, and fostering a culture grounded in ownership, collaboration, and accountability.

We employed over 26,000 permanent employees globally across manufacturing, commercial, research and development, and enabling functions. Capability building remained a key priority during the year. Employees collectively logged over 1.5 million learning hours through a mix of digital, classroom, experiential, and on-the-job learning programs, reaffirming our emphasis on continuous learning and upskilling. Leadership development received focused attention through structured programs such as RISE, ENHANCE, and COMPASS, designed to strengthen leadership readiness, coaching capability, succession pipelines, and cross-functional collaboration across frontline, middlemanagement, and senior leadership levels.

Upholding our commitment to building a future-ready organization, we strengthened our people practices, focusing on inclusion, safety, and employee engagement. Our DEI initiatives, aided by mentoring programs and inclusive hiring practices, progressed steadily, contributing to improved workforce representation and a more inclusive work environment.

Workplace safety and employee well-being are priorities across our manufacturing and commercial locations. Through our WellBeing360 framework, we delivered over 210 wellness interventions across 13 locations covering physical, emotional, nutritional and financial well-being. We also fortified our Occupational Health and Safety systems through structured risk assessments, training programs, preventive measures, and regular audits across manufacturing facilities. Industrial relations across all manufacturing sites remained stable and constructive, supported by regular engagement with employee representatives, transparent communication, and effective grievance redressal mechanisms.

We further deepened employee engagement through Town halls, feedback platforms, mentoring initiatives, and leadership interactions. During the year, Lupin achieved global Great Place To Work® certification, with 85% employee participation and 85% positive responses across engagement and workplace culture parameters, reinforcing the strength of our people-centric and value-driven culture.

Read more in the Human Capital chapter on page 131.

Key Financial Ratios

In accordance with the provisions of Schedule V of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, we have provided details of significant variations in key financial ratios. A change of 25% or more compared to the immediately preceding financial year, along with explanations for such changes, has been disclosed as part of the Standalone Financial Statements.

These movements primarily reflect changes in operating performance, cost structure, capital allocation, and market conditions across geographies. The relevant disclosures, together with management explanations, are provided to enhance transparency and enable stakeholders to better understand year-on-year trends in financial performance.

The detailed statement of key financial ratios and related commentary is included in Note 65 of the Standalone Financial Statements.

Disclosure of Accounting Treatment

The financial statements for the year ended March 31, 2026, have been prepared in accordance with the Indian Accounting Standards (Ind AS) notified under Section 133 of the Companies Act, 2013, read together with the relevant rules issued thereunder and other applicable provisions of the Act. There has been no deviation from the prescribed accounting treatment in the preparation of these financial statements. All accounting policies have been applied consistently across periods and are aligned with applicable Ind AS requirements, ensuring a true and fair view of the company’s financial performance and position.

India

Catalyzing Health in India

8th

Rank in Indian Pharmaceutical Market (IPM)

30%

Contribution to Lupin’s Global Revenues

5

Lupin Brands Ranked among the Top 300 Brands in India

India is at the heart of Lupin’s story. It is our largest market, our deepest source of patient trust, and the foundation on which we continue to build global capabilities. Above all, it is where our values of care, customer focus, and passion for excellence are translated into everyday patient impact. As healthcare needs evolve and chronic diseases become more prevalent, our role has expanded beyond supplying medicines to building trusted brands, advancing therapeutic leadership and supporting patients across their care journey. Through this, we bring our purpose to life – to catalyze treatments that transform hope into healing.

While the Indian Pharmaceutical Market (IPM) grew 9.9% in FY26, Lupin India grew 10.5%, continuing to outperform the market, with chronic therapies driving growth. We retained our 8th position in the IPM (IQVIA MAT, March 2026), while five of our brands ranked among India’s top 300. These milestones reflect the trust placed in Lupin by physicians and patients, the strength of our brands, and the relevance of our therapy-led strategy. They also reaffirm India as both a growth engine and a strategic capability hub for Lupin, strengthening our leadership at home while supporting our ambition to deliver high-quality healthcare globally.

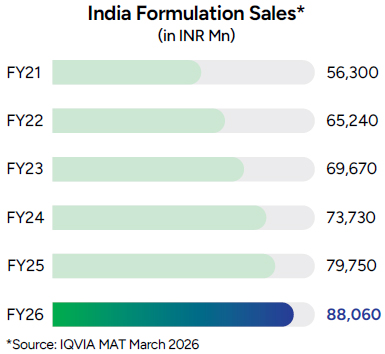

India Formulation Performance

Our India Region Formulations (IRF) business delivered another year of resilient growth in FY26, with revenues of INR 88,060 million, continuing its strong growth trajectory. The India market contributed 30% to our global revenues, underscoring its importance as both a growth engine and a strategic capability base. Our branded business grew 11.7%, outperforming the Indian Pharmaceutical Market (IPM) by 180 basis points.

During FY26, our India business further strengthened its leadership in the domestic formulations market, driven by growth in chronic therapies, science-led partnerships, differentiated offerings , and differentiated products. We also expanded our presence in high-growth cardiometabolic therapies while reinforcing our leadership in respiratory care and sustainable healthcare solutions.

A key focus during the year was the expansion of our cardiometabolic portfolio, particularly in the GLP-1 segment, reflecting the growing burden of diabetes and obesity in India. We entered into an exclusive licensing, supply, and distribution agreement with Gan & Lee Pharmaceuticals for Bofanglutide, a novel fortnightly GLP-1 receptor agonist.

The agreement gives Lupin exclusive commercialization rights in India and strengthens our presence in next-generation therapies for diabetes and obesity.

We also entered into a licensing and supply agreement with Zydus Lifesciences to co-market an innovative semaglutide injection in India. This partnership will broaden patient access to advanced metabolic therapies.

These partnerships reflect our disciplined approach to portfolio expansion – bringing differentiated therapies to patients faster while strengthening our presence in high-value chronic care segments.

Overall, the India business continued to build momentum through new product introductions, expansion in chronic therapies and a differentiated product mix. We are building a high-value, innovation-led portfolio anchored in chronic disease management and supported by strategic partnerships, advanced therapies, and sustainable product innovation. These investments position Lupin to address India’s evolving healthcare needs with trusted, science-led medicines while creating sustainable long-term value.

With leadership in chronic therapies, a growing innovation portfolio and expanding capabilities in next-generation medicines, India remains both Lupin’s largest growth market and the foundation for building healthcare solutions with global relevance.

Therapy‑Wise Mix and Strategic Focus

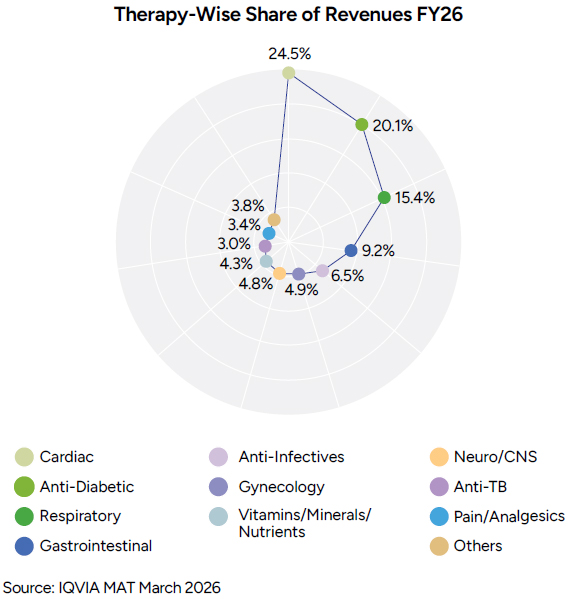

Chronic therapies now account for approximately 66% of our branded India Formulations revenues, up from 64% in FY25, reflecting the growing importance of long-term disease management. Cardiology remains our largest therapy area, followed by anti-diabetics, respiratory, gastroenterology, and anti-infectives. Together, these therapies contribute approximately 75% of revenues, providing a resilient and sustainable foundation for growth.

In FY26, our key priority therapies outperformed the market, reflecting the strength of our brands, deep physician engagement, and the depth of our field presence. Cardiology led growth at 18.9%, while anti-diabetes continued to outperform the market, supported by core brands and line extensions. Our respiratory franchise grew by more than 20%, despite seasonal variability, while Neuro/CNS and gastroenterology also delivered strong growth through broader physician coverage and a more relevant portfolio.

This performance reflects years of disciplined portfolio building and sustained investment in our priority therapies. During the year, our field force engaged with more than 400,000 healthcare professionals, strengthening prescription continuity and reinforcing physician confidence in our core brands. In cardiology and anti-diabetes, growth was driven by deeper prescription penetration and sustained demand. Across both therapies, we recorded mid-to-high single-digit volume growth, supported by three new line extensions and focused brand investments. Our diabetes portfolio also benefited from the integration of past acquisitions, enabling us to serve patients better.

In respiratory, patient education, scientific engagement, and brand reinforcement helped sustain demand across both acute and maintenance therapies despite pricing pressure and competitive intensity.

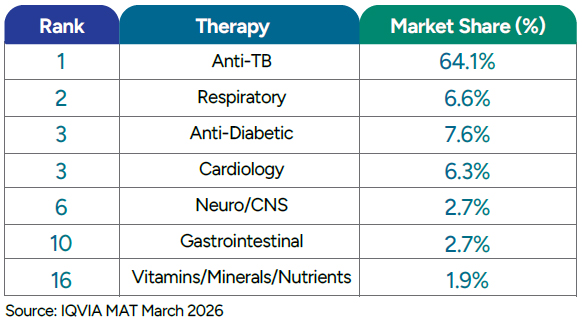

We strengthened our leadership in anti-tuberculosis therapies, increasing market share to 64.1% from 61.3% in FY25. Other priority segments, including neuro/CNS, VMN, and gastroenterology, also contributed to growth and portfolio diversification. Selective brand investments expanded physician reach and improved field-force productivity.

We also expanded our presence across Tier-2 and Tier-3 markets, improving access to both chronic and acute therapies while creating new opportunities for brand expansion and long-term portfolio growth.

Lupin’s Focused Therapy-Wise Ranking

Advancing Therapy Leadership Through Science, Digital Engagement, and Field Excellence

Our leadership across therapies is supported not only by strong brands but also by sustained investments in medical education, digital engagement, and field excellence. During FY26, more than 73,500 healthcare professionals participated in our scientific education programs, while over 980,000 patients benefited from disease awareness and adherence initiatives.

Our field force remains a key competitive advantage, enabled by digital platforms such as SmartRep and Sahayak, which enhance productivity, personalize physician engagement, and strengthen scientific dialogue. Complementing these efforts, patient-support programs such as HuMrahi, JAI, and other screening initiatives improve treatment adherence, promote early diagnosis, and support better health outcomes across multiple therapy areas. Together, these capabilities deepen physician engagement, strengthen prescription continuity, reinforce Lupin’s leadership across therapies, and bring better patient outcomes.

Patient Support Programs

Patient-centricity is integral to our strategy. Beyond developing medicines, we work to support patients across the care continuum through initiatives that promote early diagnosis, improve access, strengthen treatment adherence, and enable long-term disease management.

During FY26, we further expanded the reach of our patient-support programs across chronic, acute, and specialty therapies, reinforcing our commitment to improving health outcomes while building stronger and more enduring relationships with patients and healthcare professionals.

During FY26, our patient support initiatives continued to focus on continuity of care, scalability, and measurable outcomes. By integrating patient education, digital tools, and collaboration with healthcare professionals, we are building care models that extend beyond treatment to improve adherence, strengthen disease management, and deliver better health outcomes. Through these efforts, we continue to bring our purpose to life – catalyzing treatments that transform hope into healing.

Accelerating Digital Transformation for Scalable Impact

Digital capabilities have become an important source of competitive advantage, enabling stronger engagement with healthcare professionals, improving field-force effectiveness and expanding patient reach. Throughout FY26, we continued to embed digital technologies across our commercial operations to improve productivity, enhance decision-making, and deliver more personalized interactions.

Our omnichannel platforms – Lupin Connect, DigiEngage, and GP Konnect enabled engagement with more than 110,000 healthcare professionals, generating over 10 million interactions during the year and significantly extending our reach beyond traditional channels.

SmartRep, our digital sales platform, continued to strengthen planning, analytics, and knowledge management across the organization. The platform now supports more than 11,000 active users, with an adoption rate exceeding 93%. Sahayak, the AI-enabled assistant integrated within SmartRep, resolved over 12,500 internal queries during the year with a 99.5% resolution rate, improving responsiveness and operational efficiency.

Anya, our AI-powered healthcare assistant, engaged more than 629,000 users by delivering content across 16 therapy areas in 20 Indian languages, while Lupin Gurukul continued to strengthen learning and knowledge sharing across commercial teams through a centralized digital platform.

Together, these investments are transforming how we engage with healthcare professionals, support our field teams and improve patient outreach. By embedding digital and AI-enabled capabilities across our commercial operations, we are building a more agile, data-driven, and scalable organization – one that is better equipped to improve health outcomes while delivering sustainable long-term growth.

India Adjacencies

Our India Adjacencies are built on a simple belief – that healthcare should extend beyond medicines to become more accessible, connected, and outcome-oriented. This philosophy is reflected across our consumer healthcare, diagnostics, digital health, and neurorehabilitation businesses, each strengthening a different part of the patient journey. From expanding diagnostic access in non-metro markets and growing trusted consumer brands to improving patient engagement through digital health and delivering measurable outcomes in neurorehabilitation, these businesses complement our pharmaceutical portfolio while addressing broader healthcare needs. Together, they strengthen Lupin’s healthcare ecosystem, deepen patient relationships, and bring our purpose to life by catalyzing treatments that transform hope into healing.

Lupin Diagnostics

Lupin Diagnostics is building a technology-enabled diagnostics network that brings high-quality, reliable testing closer to patients. As India’s diagnostics market evolves from a fragmented landscape to an integrated healthcare ecosystem, our strategy is to combine scientific excellence, digital capabilities, and national reach to improve diagnostic accuracy, accessibility, and clinical outcomes.

Since its launch in 2021, Lupin Diagnostics has established a pan-India network comprising the National Reference Laboratory (NRL) in Navi Mumbai, 50 processing laboratories, 808 collection centers, and 3,000+ clinics across more than 250 locations, spanning metros as well as Tier-1, Tier-2, Tier-3, and select Tier-4 towns. Today, the network serves over 200,000 patients each month, enabling faster sample movement, improved network efficiency, and dependable access across urban and non-urban markets. These investments contributed to a 44% increase in gross revenues during FY26. Notably, 60% of testing volumes originated from non-metro markets, reflecting our commitment to expanding access to quality diagnostics.

Quality remains the foundation of our diagnostics business. All laboratories operate in accordance with national and international quality standards, while our greenfield laboratories comply with ISO 15189:2022. Importantly, every laboratory in our network is accredited by the National Accreditation Board for Testing and Calibration Laboratories (NABL), reinforcing our commitment to accuracy, reliability, and patient confidence.

Our 45,000 sq. ft. NRL serves as the scientific backbone of the network and supports advanced diagnostics across oncology, neurology, gastroenterology, gynecology, IVF, endocrinology, and precision medicine. It is equipped with sophisticated proficiencies including Next-Generation Sequencing (NGS), AI-based automated karyotyping, high-throughput immunoassays, automated histopathology and immunohistochemistry (IHC), along with high-end capabilities in flow cytometry and microbiology.

With a specialized focus on gynecology and IVF diagnostics, its offerings include FMF-approved maternal screening, Non-Invasive Prenatal Testing (NIPT), Pre-implantation Genetic Testing (PGT) and many more tests. These capabilities have positioned Lupin Diagnostics among the leading providers of gynecology diagnostic services in India.

Advanced and specialty diagnostics accounted for 17% of test revenues during FY26, reflecting our continued shift towards higher-value and more complex testing.

During the year, we expanded our test portfolio across oncology, neurology, gastroenterology, gynecology, IVF, and preventive healthcare while extending access to specialized diagnostics in underserved markets. Enhanced digital reporting – integrating trend analysis, risk indicators, and preventive insights – improved clinical interpretation and patient engagement, with all reports delivered digitally.

Operational excellence remains central to our model. More than 500 trained field executives manage temperature-controlled sample logistics with standardized handling protocols, reducing sample rejection rates while strengthening end-to-end traceability through technology-enabled monitoring and structured quality audits.

As the network continues to scale, we remain focused on improving utilization, increasing network density, and enhancing operating leverage. Together with Lupin’s broader healthcare ecosystem, Lupin Diagnostics is well positioned to play an increasingly important role in enabling earlier diagnosis, better clinical decisions, and improved patient outcomes.

LupinLife Consumer Healthcare

During FY26, we took an important strategic step by carving out our consumer health business into a wholly owned subsidiary – LupinLife Consumer Healthcare Limited (LCH), effective July 1, 2025. This realignment provides greater strategic focus and positions the business to capture the long-term opportunity in India’s rapidly expanding self-care and wellness market.

Since its launch in 2017, LupinLife has built a trusted portfolio of science-backed consumer healthcare brands, including Softovac®, Aptivate®, Beplex® Forte and Corcium®, addressing everyday health and wellness needs.

Softovac® and Aptivate® continue to anchor the portfolio as category-leading brands. Softovac® retained its leadership in the bulk laxatives segment, sustaining a market share of over 40% while delivering steady volume growth during FY26. Despite category headwinds, Aptivate® maintained resilient performance, supported by strong caregiver engagement and focused brand activation.

During the year, we further strengthened the portfolio through the addition of the Corcium® range and Beplex® Forte, broadening our presence in the wellness category. Investments in brand building, packaging innovation, consumer communication, and channel-specific activation helped expand retail reach and strengthen market visibility.

LupinLife now reaches approximately 10 million households through a diversified omnichannel presence spanning traditional trade, modern retail, and digital commerce. During FY26, the business expanded its retail footprint by 50% while investing in automation and data-driven capabilities to enhance commercial execution, improve decision-making, and support scalable long-term growth.

Lupin Digital Health

Lupin Digital Health (LDH) builds on our therapy leadership to deliver continuous, technology-enabled care by integrating clinical science, digital therapeutics, and behavioral interventions into structured disease management pathways.

LYFE®, our flagship digital health platform, enables continuous care across the patient journey – from prevention and monitoring to rehabilitation and chronic disease management. During FY26, the platform supported more than 15,000 patients through a growing ecosystem of hospitals, leading insurers, med-tech partners and a network of 1,000 healthcare professionals. Growth accelerated during the year, driven by strong adoption across hospital networks, with signed units expanding nearly sixfold year-on- year and patient volumes registering a significant uplift.

Patient engagement remains a defining strength of the platform. Approximately 94% of enrolled patients completed their programs, while Net Promoter Scores improved to 86%, reflecting high levels of patient satisfaction and continuity of care. Through 17 structured clinical touchpoints and more than 200 disease cohorts, LYFE® delivers personalized care pathways tailored to individual risk profiles and comorbidities.

Anchored in clinical quality and patient safety, LYFE® adheres to global cardiology guidelines. It operates as a CDSCO-licensed Class C Software as a Medical Device (SaMD) and is supported by ISO 13485:2016 and ISO 27001 certifications, ensuring robust clinical governance, cybersecurity and regulatory compliance.

LDH continues to demonstrate robust clinical outcomes. Hospitalization rates have reduced by approximately 50% across study cohorts, underscoring the effectiveness of digitally enabled cardiac rehabilitation.

LYFE® also delivers tangible economic value for healthcare providers. Adoption across leading hospital chains has resulted in a 3-4% uplift in cardiac department revenues and a 4-5% increase in EBITDA, without incremental cost. Structured post-discharge care extends engagement beyond hospitalization through timely follow-ups, diagnostics, and pharmacy support, while helping providers limit patient attrition.

Looking ahead, LDH will continue to expand across hospitals, insurers and employer ecosystems while extending its capabilities into respiratory, diabetes and oncology care. By combining clinical expertise, digital intelligence, and data-driven care pathways, we are building a scalable healthcare platform that enables earlier intervention, improves patient outcomes, and strengthens continuity of care across the healthcare ecosystem.

Atharv Ability

Neurorehabilitation remains one of the most underserved areas of healthcare in India. While patients often receive timely acute treatment, many face a significant gap in structured rehabilitation after discharge, limiting their ability to regain functional independence. Atharv Ability was established to bridge this gap through integrated, technology-enabled neurorehabilitation that supports recovery across the continuum of care.

Our centers in Mumbai and Hyderabad, with a third center recently opened in Delhi, provide multidisciplinary outpatient rehabilitation that combines clinical expertise with advanced rehabilitation technologies. Built on global best practices, Atharv Ability brings together physiotherapy, occupational therapy, speech therapy, cognitive behavioral therapy, aquatic therapy, and pain management within a single integrated care model. The centers support patients recovering from stroke, traumatic brain and spinal cord injuries, Parkinson’s disease, Alzheimer’s disease, multiple sclerosis, cerebral palsy, and autism spectrum disorders.

Technology-enabled rehabilitation remains a key differentiator. Individualized treatment pathways, supported by advanced robotic rehabilitation and structured clinical outcome measures, focus on restoring functional independence rather than simply managing symptoms. During FY26, Atharv Ability delivered approximately 52,000 therapy sessions, including more than 9,000 robotic rehabilitation sessions and over 3,000 aquatic therapy sessions. More importantly, over 5,000 patients demonstrated measurable improvements in mobility, coordination, functional ability and activities of daily living, reinforcing the effectiveness of our integrated rehabilitation model.

Beyond clinical outcomes, Atharv Ability enables patients to return to work, education and independent living, improving both quality of life and long-term social participation. It exemplifies our purpose of transforming hope into healing, translated into a replicable, outcome-oriented care model with tangible functional and societal impact.

Lupin Life Sciences Limited

Lupin Life Sciences Limited (LLSL), our trade generics business, completed its first full year of operations following its carve-out as a wholly owned subsidiary in July 2024. The business was established to expand access to high-quality, affordable medicines by serving India’s fast-growing trade generics market through a dedicated operating model.

During FY26, LLSL focused on building a scalable commercial platform by strengthening chemist engagement, expanding its field presence and broadening its distribution network. More than 350 business executives engaged over 120,000 chemists, laying a strong foundation for long-term growth and deeper market penetration.

With the trade generics market expected to grow at 12-15% CAGR over the next five years, LLSL is expanding its presence across Tier-2 and smaller towns, where demand for quality affordable medicines continues to rise.

During the year, the business shifted from a stockist-led distribution model to a chemist-led demand generation strategy, improving retail reach and driving growth across key therapeutic areas including pain management, anti-infectives, gastroenterology, respiratory care, dermatology and multivitamins.

While FY26 was a year of transition and capability building, the business enters FY27 with a stronger commercial organization, a broader distribution footprint and a sharper brand-building strategy. We believe LLSL is well positioned to accelerate growth while advancing Lupin’s broader purpose of improving access to trusted, high-quality medicines across underserved markets.

United States

Catalyzing Innovation in the U.S.

3rd

Largest Generics Company (by Filled Prescriptions)

42%

Contribution to Global Revenues

50+

Products Rank #1 in the U.S. (in Respective Categories)

The U.S. remains a pivotal hub within the global pharmaceutical industry. Driven by cutting-edge scientific innovation, a mature healthcare infrastructure, and a consistent demand for affordable treatments, the market presents substantial opportunities for continued expansion. Over the years, Lupin has pursued disciplined investments to shape a distinctive portfolio and build strong capabilities. Driven by our purpose of catalyzing treatments that transform hope into healing and expanding patient access to trusted, cost-efficient therapies, we are well-positioned to sustain momentum and deliver accessible, differentiated healthcare solutions that enhance the quality of life for patients.

Our U.S. business delivered a strong performance in FY26, with revenues of USD 1,318 million, reflecting a growth of 40% and contributing 42% to Lupin’s consolidated global revenue. This performance was driven by a series of new product launches, including exclusivity-led opportunities, and the realization of sustained investments in product innovation over the years.

We are strengthening our U.S. business with a clear focus on complexity, reliability, and customer trust, facilitating broader access to essential therapies and reinforcing our purpose of catalyzing treatments that transform hope into healing.

Spiro Gavaris,

President – U.S. Generics

40%

FY26 delivered exceptional performance in the U.S., with revenue growth of

U.S. Generics Business

Lupin retained its position as the third-largest pharmaceutical company by prescriptions in both the U.S. generics and overall U.S. pharmaceutical markets by prescriptions in FY26. Our leadership strengthened further, with 61 marketed generics ranked #1, up from 48 in FY25, and 112 products among the top three in their respective categories. Our U.S. generics portfolio expanded to 151 products from 138 in FY25, further strengthening our market presence. This momentum underscores the depth of our portfolio, the steady advancement of our pipeline, and sustained business traction.

Launched in May 2025, Tolvaptan was a significant driver of the FY26 performance, benefiting from its exclusive first-to-file status and 180-day drug exclusivity. Mirabegron Extended-Release Tablets built on the momentum set in FY25 and gained in both market share and absolute value terms.

Complex injectables were an important contributor to our momentum. The launch of Risperidone long-acting injectable in the U.S., with a 180-day Competitive Generic Therapy (CGT) exclusivity, marked a key inflection point in our long-acting injectable platform. This was reinforced by the approvals and launches of Liraglutide and Glucagon Injections. Collectively, these expanded our footprint in complex injectables and improved the overall mix of our portfolio.

Respiratory generics added meaningful depth, with Tiotropium Bromide Inhalation Powder. It was the first FDA-approved generic to Spiriva® HandiHaler® in the U.S. and the first dry-powder inhaler approval from India for the U.S. market.

While pricing pressure remained evident in commoditized segments, the impact of price erosion was offset by healthy volume growth and a more favorable product mix. In FY26, we filed 11 products and launched 15, strengthening our launch cadence. Notable introductions included complex injectables such as RLD Risperdal Consta®, which secured Competitive Generic Therapy exclusivity and became the first product from our proprietary Nanomi platform. Over the next three years, we expect to bring 50+ products to market in the U.S., including exclusive first-to-file opportunities, biosimilars, as well as 505(b)(2) products.

Biosimilars emerged as a significant growth avenue for the U.S. business in FY26. We secured our first biosimilar approval from the U.S. FDA in December 2025 for Armlupeg™, a biosimilar to Neulasta® (Pegfilgrastim) – a long-acting therapy that reduces the risk of infection in patients undergoing chemotherapy. In FY27, we will advance this direction through further biosimilar approvals, targeted provider engagement, disciplined lifecycle management, and expanded patient access. Strategic collaborations will further enhance the commercialization of biosimilars with strong execution and market relevance.

Specialty Business

Respiratory care continues to be integral to us, bringing together patient need, scientific depth, device performance, and provider engagement. The business is shaped by focused brands, thoughtfully managed channels, and close partnerships with healthcare professionals.

Following our acquisition of all rights to Xopenex HFA® and Brovana® from Sunovion in 2022, Xopenex HFA® has become our lead specialty respiratory brand in the U.S. During FY26, we enhanced the precision of our execution for Xopenex HFA®, making it more targeted and evidence-led. We broadened digital engagement, strengthened brand contracting and patient support initiatives, and focused outreach toward allergists, pulmonologists, physicians, and nurses. We commenced lifecycle management initiatives aimed at improving device performance, ensuring supply reliability, and driving cost efficiency.

Our Specialty business is moving toward a more purposeful trajectory, led by respiratory therapies and ophthalmology assets complementing our acquired portfolio in Europe.

Anchored in patient impact and inspired by our purpose, our specialty strategy brings together brands, programs, and partnerships that advance care, broaden access, and generate enduring value for patients and healthcare systems.

Claus Jepsen,

President – Global Specialty

Infrastructure and Strategic Investments

Lupin’s infrastructure and capital commitments are geared toward enhancing competitiveness in complex and specialty products, while reinforcing oversight across the value chain. We invested approximately USD 250 million in our Coral Springs, Florida facility, significantly expanding manufacturing and development capabilities for complex and specialty products. This is expected to enhance local manufacturing capabilities in respiratory therapies where access, reliability, and speed are critical for patients.

Our infrastructure investment strategy is structured around two core imperatives. We evaluate selective inorganic opportunities and commercial-stage assets across the pipeline, anchored in strategic alignment, rigorous return metrics, and execution capability. We are also advancing our organic pipeline, with a focus on unmet needs and opportunities that offer meaningful therapeutic and commercial distinction.

Respiratory, neuroscience, and ophthalmology have emerged as priority therapeutic segments for sustained leadership and growth. Our programs across selective acquisitions and pipeline development are underpinned by strong cash generation and balance sheet strength, positioning us to advance value-accretive opportunities with financial discipline.

Outlook

The U.S. pharmaceuticals market enters FY27 with favorable industry dynamics, led by steady demand for accessible, high-quality medicines, an active product approval environment and growing acceptance of complex generics and biosimilars. Regulatory support for lower-cost biologic alternatives and high-barrier generics is expected to open attractive value pools for companies with deep science, agile manufacturing, and strong market access capabilities. For us, FY27 provides a meaningful runway to translate recent expansions and focused investments into a more differentiated business, led by respiratory, complex injectables, and biosimilars.

Way Forward

Looking ahead, we are focused on doubling the share of complex products in our U.S. business through respiratory products, complex injectables, 505(b)(2) products, and biosimilar launches. We will continue to expand our specialty portfolio through internal innovation complemented by selective acquisitions. Anchored in our focus on improving patient access and outcomes, and supported by strong manufacturing and launch capabilities, we are well-positioned to sustain momentum and further strengthen our leadership in the U.S. market.

Other Developed Markets

Catalyzing Global Growth

4th

Largest Generics Player in Australia

11%

Contribution to Global Revenues

~250,000

Patients in the U.K. Use Luforbec® Every Month

Our Other Developed Markets, comprising Europe, Australia, and Canada, play a key role within Lupin’s global portfolio. Our engagement across these markets is shaped by an unwavering commitment to enabling dependable access to high-quality therapies, aligned with our purpose.

Contributing to 11% of Lupin’s global revenue, these geographies operate in mature, highly regulated healthcare systems where outcomes are shaped by product differentiation, quality, supply reliability, pricing discipline, and regulatory execution.